Bank Churn Exploration and Binary Classification

Contents

1. Introduction

In this notebook we will explore a synthetic bank customer churn dataset used in a Kaggle community prediction competition, treating this like a real world problem and avoiding the use of any performance-boosting tricks that is are only specific to this competition dataset (i.e. utilizing data leakages due to the syntheticity of the data)

Churn - What and why?

Customer churn is a measure of how many customers leave the bank entirely. Customers may leave the bank due to many different reasons, a few common ones are: <ol> <li>Dissatisfaction with the products offered.</li> <li>Competitor offerings are more appealing.</li> <li>External factors that make it impossible for the customer to continue using the bank services.</li> </ol>

2. Data Cleaning

# Import packages and set styles

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.preprocessing import MinMaxScaler, LabelEncoder

from sklearn.model_selection import train_test_split, GridSearchCV, KFold, cross_val_score

from sklearn.linear_model import LogisticRegression

from sklearn.ensemble import RandomForestClassifier

from xgboost import XGBClassifier

from lightgbm import LGBMClassifier

from sklearn.ensemble import VotingClassifier

from sklearn.pipeline import Pipeline

from sklearn.base import BaseEstimator, TransformerMixin

from sklearn.cluster import KMeans

from sklearn.metrics import classification_report, confusion_matrix, accuracy_score, f1_score, auc, roc_curve, roc_auc_score, make_scorer

import warnings

warnings.filterwarnings('ignore')

plt.style.use('fivethirtyeight')

sns.set_palette("muted")

df = pd.read_csv('train.csv')

df.head()

| id | CustomerId | Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | Exited | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 15674932 | Okwudilichukwu | 668 | France | Male | 33.0 | 3 | 0.00 | 2 | 1.0 | 0.0 | 181449.97 | 0 |

| 1 | 1 | 15749177 | Okwudiliolisa | 627 | France | Male | 33.0 | 1 | 0.00 | 2 | 1.0 | 1.0 | 49503.50 | 0 |

| 2 | 2 | 15694510 | Hsueh | 678 | France | Male | 40.0 | 10 | 0.00 | 2 | 1.0 | 0.0 | 184866.69 | 0 |

| 3 | 3 | 15741417 | Kao | 581 | France | Male | 34.0 | 2 | 148882.54 | 1 | 1.0 | 1.0 | 84560.88 | 0 |

| 4 | 4 | 15766172 | Chiemenam | 716 | Spain | Male | 33.0 | 5 | 0.00 | 2 | 1.0 | 1.0 | 15068.83 | 0 |

df.shape

(165034, 14)

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 165034 entries, 0 to 165033

Data columns (total 14 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 id 165034 non-null int64

1 CustomerId 165034 non-null int64

2 Surname 165034 non-null object

3 CreditScore 165034 non-null int64

4 Geography 165034 non-null object

5 Gender 165034 non-null object

6 Age 165034 non-null float64

7 Tenure 165034 non-null int64

8 Balance 165034 non-null float64

9 NumOfProducts 165034 non-null int64

10 HasCrCard 165034 non-null float64

11 IsActiveMember 165034 non-null float64

12 EstimatedSalary 165034 non-null float64

13 Exited 165034 non-null int64

dtypes: float64(5), int64(6), object(3)

memory usage: 17.6+ MB

Column descriptions for the features within the dataset

- Customer ID: A unique identifier for each customer

- Surname: The customer’s surname or last name

- Credit Score: A numerical value representing the customer’s credit score

- Geography: The country where the customer resides (France, Spain or Germany)

- Gender: The customer’s gender (Male or Female)

- Age: The customer’s age.

- Tenure: The number of years the customer has been with the bank

- Balance: The customer’s account balance

- NumOfProducts: The number of bank products the customer uses (e.g., savings account, credit card)

- HasCrCard: Whether the customer has a credit card (1 = yes, 0 = no)

- IsActiveMember: Whether the customer is an active member (1 = yes, 0 = no)

- EstimatedSalary: The estimated salary of the customer

- Exited: Whether the customer has churned (1 = yes, 0 = no)

print(df.duplicated().sum())

print(df.isna().sum())

0

id 0

CustomerId 0

Surname 0

CreditScore 0

Geography 0

Gender 0

Age 0

Tenure 0

Balance 0

NumOfProducts 0

HasCrCard 0

IsActiveMember 0

EstimatedSalary 0

Exited 0

dtype: int64

On the surface it appears that there are no duplicates in this dataset, however looking deeper we see that the CustomerId column which is supposed to be a unique identifier for each customer is apparently not so unique after all!

df[df['CustomerId'].duplicated()]

| id | CustomerId | Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | Exited | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 99 | 99 | 15673599 | Williamson | 618 | Spain | Male | 35.0 | 5 | 133476.09 | 1 | 0.0 | 1.0 | 154843.40 | 0 |

| 113 | 113 | 15690958 | Palerma | 594 | France | Male | 35.0 | 2 | 185732.59 | 1 | 1.0 | 1.0 | 155843.48 | 0 |

| 122 | 122 | 15606887 | Olejuru | 762 | France | Male | 29.0 | 8 | 0.00 | 2 | 1.0 | 0.0 | 43075.70 | 0 |

| 124 | 124 | 15741417 | Ts'ui | 706 | France | Female | 42.0 | 8 | 0.00 | 2 | 1.0 | 0.0 | 167778.61 | 0 |

| 160 | 160 | 15763612 | Y?an | 712 | France | Female | 43.0 | 4 | 0.00 | 2 | 0.0 | 0.0 | 117038.96 | 0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 165029 | 165029 | 15667085 | Meng | 667 | Spain | Female | 33.0 | 2 | 0.00 | 1 | 1.0 | 1.0 | 131834.75 | 0 |

| 165030 | 165030 | 15665521 | Okechukwu | 792 | France | Male | 35.0 | 3 | 0.00 | 1 | 0.0 | 0.0 | 131834.45 | 0 |

| 165031 | 165031 | 15664752 | Hsia | 565 | France | Male | 31.0 | 5 | 0.00 | 1 | 1.0 | 1.0 | 127429.56 | 0 |

| 165032 | 165032 | 15689614 | Hsiung | 554 | Spain | Female | 30.0 | 7 | 161533.00 | 1 | 0.0 | 1.0 | 71173.03 | 0 |

| 165033 | 165033 | 15732798 | Ulyanov | 850 | France | Male | 31.0 | 1 | 0.00 | 1 | 1.0 | 0.0 | 61581.79 | 1 |

141813 rows × 14 columns

df.loc[df['CustomerId']==15732798]

| id | CustomerId | Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | Exited | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 62381 | 62381 | 15732798 | H? | 733 | France | Female | 35.0 | 6 | 0.00 | 2 | 1.0 | 1.0 | 52301.15 | 0 |

| 83124 | 83124 | 15732798 | Chukwubuikem | 607 | Germany | Female | 53.0 | 5 | 121490.04 | 1 | 0.0 | 0.0 | 101039.76 | 1 |

| 139366 | 139366 | 15732798 | Hsueh | 652 | Germany | Male | 28.0 | 1 | 171770.43 | 2 | 0.0 | 1.0 | 153373.50 | 0 |

| 156934 | 156934 | 15732798 | Hsueh | 637 | France | Male | 32.0 | 1 | 121520.41 | 1 | 1.0 | 1.0 | 77965.49 | 0 |

| 165033 | 165033 | 15732798 | Ulyanov | 850 | France | Male | 31.0 | 1 | 0.00 | 1 | 1.0 | 0.0 | 61581.79 | 1 |

We see that there are multiple different customers associated with the above CustomerId. We can tell that they are most likely different individuals carrying different surnames/living in different countries/are of different genders.

To investigate further we shall apply a group by condition to make the condition more specific

df[df[['CustomerId', 'Surname', 'Geography', 'Gender']].duplicated()]

| id | CustomerId | Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | Exited | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 779 | 779 | 15718773 | Pisano | 605 | France | Female | 37.0 | 0 | 0.00 | 2 | 1.0 | 1.0 | 160129.99 | 0 |

| 1132 | 1132 | 15694272 | Nkemakolam | 665 | France | Male | 38.0 | 1 | 0.00 | 1 | 1.0 | 0.0 | 77783.35 | 0 |

| 1280 | 1280 | 15626012 | Obidimkpa | 459 | France | Male | 48.0 | 3 | 0.00 | 1 | 1.0 | 1.0 | 50016.17 | 1 |

| 1340 | 1340 | 15589793 | Onwuamaeze | 633 | France | Male | 53.0 | 1 | 0.00 | 2 | 1.0 | 1.0 | 190998.96 | 0 |

| 1387 | 1387 | 15598097 | Johnstone | 651 | France | Male | 44.0 | 9 | 0.00 | 2 | 1.0 | 0.0 | 26257.01 | 0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 164974 | 164974 | 15774882 | Mazzanti | 687 | Germany | Female | 35.0 | 3 | 99587.43 | 2 | 1.0 | 1.0 | 1713.10 | 0 |

| 164977 | 164977 | 15704466 | Udokamma | 548 | France | Female | 34.0 | 2 | 0.00 | 2 | 0.0 | 1.0 | 195074.62 | 0 |

| 164982 | 164982 | 15592999 | Fang | 535 | France | Female | 42.0 | 6 | 0.00 | 1 | 0.0 | 1.0 | 185660.30 | 1 |

| 164983 | 164983 | 15694192 | Nwankwo | 598 | France | Female | 38.0 | 6 | 0.00 | 2 | 0.0 | 0.0 | 173783.38 | 0 |

| 165006 | 165006 | 15627665 | Sung | 614 | France | Female | 39.0 | 4 | 0.00 | 2 | 1.0 | 1.0 | 74379.57 | 0 |

19154 rows × 14 columns

df.loc[(df['CustomerId']==15627665)&(df['Surname']=='Sung')&(df['Geography']=='France')]

| id | CustomerId | Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | Exited | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 16987 | 16987 | 15627665 | Sung | 614 | France | Male | 46.0 | 0 | 0.0 | 1 | 1.0 | 1.0 | 74379.57 | 0 |

| 22713 | 22713 | 15627665 | Sung | 642 | France | Female | 60.0 | 8 | 0.0 | 2 | 1.0 | 1.0 | 74379.57 | 0 |

| 165006 | 165006 | 15627665 | Sung | 614 | France | Female | 39.0 | 4 | 0.0 | 2 | 1.0 | 1.0 | 74379.57 | 0 |

Picking CustomerId 15627665 which met the group by condition we see that it is associated with 2 customers that share the same surname, country, and gender. However, looking at the Age we see that they are 21 years apart, with tenures short enough that we cannot say they are the same individual enrolled in the bank’s services at different points in her life.

Looking at the data we have and any additional information/data dictionary from the data source we can conclude that there is not enough information for us to treat similar CustomerIds as a single customer. Hence in this notebook we will proceed as if each row is a unique customer.

In reality if working with banks such an error in the data should not occur due to strict regulations and scrutiny they are subjected to. If it does happen, a thorough investigation should happen and we can seek further clarity on the dataset accordingly.

3. Exploratory Data Analysis

num_cols = df.select_dtypes(exclude='object').columns

cat_cols = df.select_dtypes('object').columns

for col in cat_cols:

print("Number of unique categories: ", df[col].nunique())

print(df[col].value_counts(), "\n---------------------------------\n")

Number of unique categories: 2797

Surname

Hsia 2456

T'ien 2282

Hs? 1611

Kao 1577

Maclean 1577

...

Samaniego 1

Lawley 1

Bonwick 1

Tennant 1

Elkins 1

Name: count, Length: 2797, dtype: int64

---------------------------------

Number of unique categories: 3

Geography

France 94215

Spain 36213

Germany 34606

Name: count, dtype: int64

---------------------------------

Number of unique categories: 2

Gender

Male 93150

Female 71884

Name: count, dtype: int64

---------------------------------

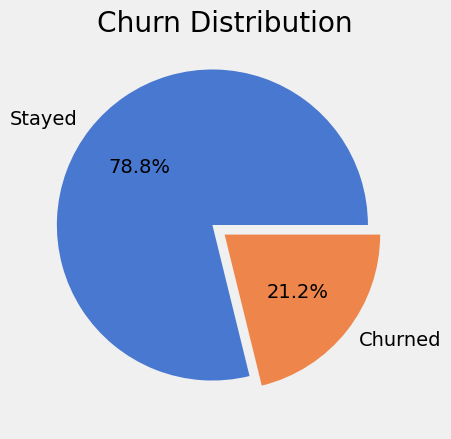

plt.pie(df['Exited'].value_counts().values, explode=(0.1,0), labels=['Stayed','Churned'], autopct='%1.1f%%')

plt.title('Churn Distribution')

plt.show()

We see that this is a slightly imbalanced dataset with our target class making up ~21.2% of the samples.

cat_cols

Index(['Surname', 'Geography', 'Gender'], dtype='object')

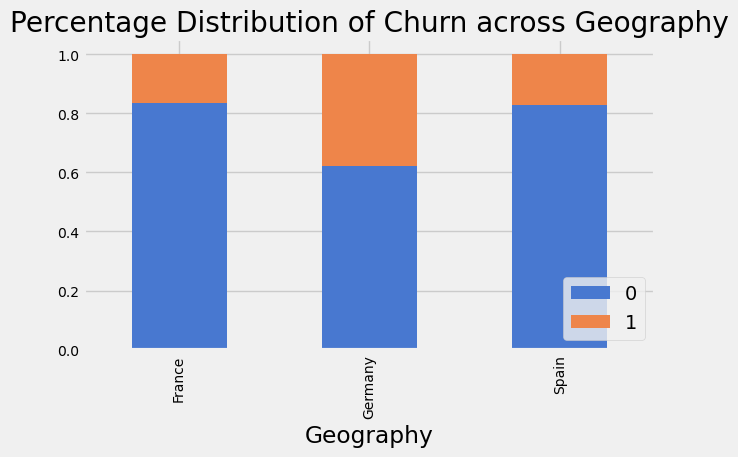

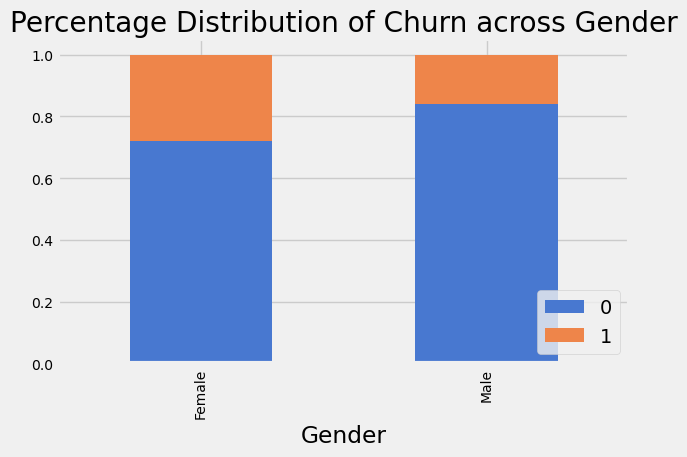

for col in cat_cols:

if col == 'Surname':

continue

xtab = pd.crosstab(df[col], df['Exited'], normalize='index')

xtab.plot(kind='bar', stacked=True, fontsize=10).legend(loc='lower right')

plt.title(f'Percentage Distribution of Churn across {col}')

plt.tight_layout()

plt.show()

Here we see that a higher proportion of customers from Germany have churned, similar behaviour is seen in Female customers across the dataset. This suggests that the features will be useful in our predictive model.

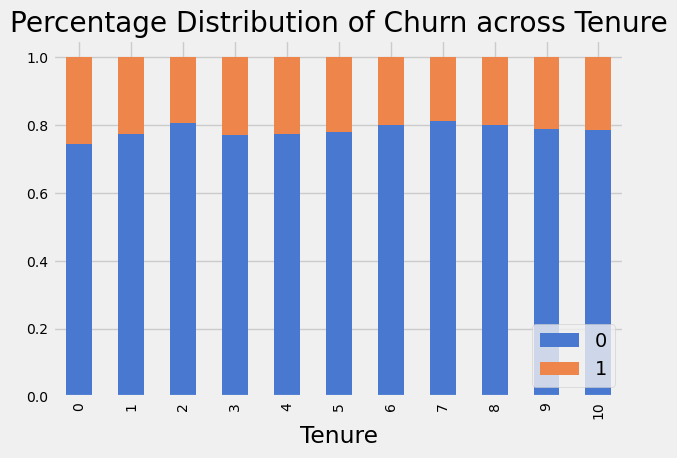

xtab = pd.crosstab(df['Tenure'], df['Exited'], normalize='index')

xtab.plot(kind='bar', stacked=True, fontsize=10).legend(loc='lower right')

plt.title(f'Percentage Distribution of Churn across Tenure')

plt.tight_layout()

plt.show()

New customer with 0 years with the bank has a slightly higher churn rate than the other customers.

pd.DataFrame(df.groupby(['HasCrCard','IsActiveMember'])[['HasCrCard','IsActiveMember']].value_counts())

| count | ||

|---|---|---|

| HasCrCard | IsActiveMember | |

| 0.0 | 0.0 | 19646 |

| 1.0 | 20960 | |

| 1.0 | 0.0 | 63239 |

| 1.0 | 61189 |

There is an even distribution among customer that have a credit card and whether they are an active member (unable to verify what this means in the context of this dataset)

In this dataset ~50% of the customers who have a credit card is active, also 50% of the customers who do not have a credit card is active. This goes against the intuition that most customers with an active credit card with the bank will most likely be using it at least occassionally. I suspect this is due to the synthetic nature of the dataset.

In reality more clarity will be required for an ambiguous feature such as IsActiveMember, such as the definition and conditions surrounding a customer being considered active. With these information further feature engineering can possible be conducted to extract more useful information out of this feature.

df.describe()

| id | CustomerId | CreditScore | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | Exited | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 165034.0000 | 1.650340e+05 | 165034.000000 | 165034.000000 | 165034.000000 | 165034.000000 | 165034.000000 | 165034.000000 | 165034.000000 | 165034.000000 | 165034.000000 |

| mean | 82516.5000 | 1.569201e+07 | 656.454373 | 38.125888 | 5.020353 | 55478.086689 | 1.554455 | 0.753954 | 0.497770 | 112574.822734 | 0.211599 |

| std | 47641.3565 | 7.139782e+04 | 80.103340 | 8.867205 | 2.806159 | 62817.663278 | 0.547154 | 0.430707 | 0.499997 | 50292.865585 | 0.408443 |

| min | 0.0000 | 1.556570e+07 | 350.000000 | 18.000000 | 0.000000 | 0.000000 | 1.000000 | 0.000000 | 0.000000 | 11.580000 | 0.000000 |

| 25% | 41258.2500 | 1.563314e+07 | 597.000000 | 32.000000 | 3.000000 | 0.000000 | 1.000000 | 1.000000 | 0.000000 | 74637.570000 | 0.000000 |

| 50% | 82516.5000 | 1.569017e+07 | 659.000000 | 37.000000 | 5.000000 | 0.000000 | 2.000000 | 1.000000 | 0.000000 | 117948.000000 | 0.000000 |

| 75% | 123774.7500 | 1.575682e+07 | 710.000000 | 42.000000 | 7.000000 | 119939.517500 | 2.000000 | 1.000000 | 1.000000 | 155152.467500 | 0.000000 |

| max | 165033.0000 | 1.581569e+07 | 850.000000 | 92.000000 | 10.000000 | 250898.090000 | 4.000000 | 1.000000 | 1.000000 | 199992.480000 | 1.000000 |

num_cols

Index(['id', 'CustomerId', 'CreditScore', 'Age', 'Tenure', 'Balance',

'NumOfProducts', 'HasCrCard', 'IsActiveMember', 'EstimatedSalary',

'Exited'],

dtype='object')

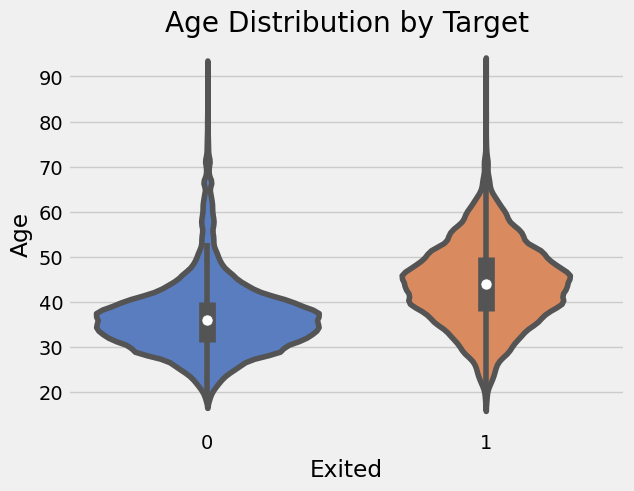

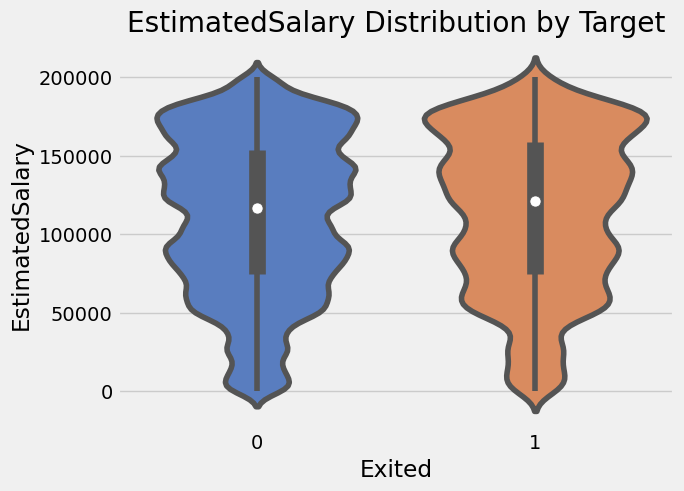

for col in num_cols:

if col in ['id','Exited','HasCrCard','Tenure','NumOfProducts','IsActiveMember']:

continue

sns.violinplot(df, x='Exited', y=col)

plt.title(f'{col} Distribution by Target')

plt.show()

The numerical features all have similar distributions between their churned and non-churned customers except for Age where we see the distribution for churned customers is centred around an older age. (~45 years old vs ~35 years old for non-churned).

# Fitting labelencoders with all the labels from train and test dataset so the label mappings are consistent

test_labels = pd.read_csv('test.csv')[['Geography','Gender','Surname']]

set_geo = set(df['Geography']).union(test_labels['Geography'])

set_gender = set(df['Gender']).union(test_labels['Gender'])

set_surname = set(df['Surname']).union(test_labels['Surname'])

le_geo = LabelEncoder()

le_gender = LabelEncoder()

le_surname = LabelEncoder()

le_geo.fit(list(set_geo))

le_gender.fit(list(set_gender))

le_surname.fit(list(set_surname))

# Encoding categorical features

df['Geography'] = le_geo.transform(df['Geography'])

df['Gender'] = le_gender.transform(df['Gender'])

df['Surname'] = le_surname.transform(df['Surname'])

df.head()

| id | CustomerId | Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | Exited | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 15674932 | 1992 | 668 | 0 | 1 | 33.0 | 3 | 0.00 | 2 | 1.0 | 0.0 | 181449.97 | 0 |

| 1 | 1 | 15749177 | 1993 | 627 | 0 | 1 | 33.0 | 1 | 0.00 | 2 | 1.0 | 1.0 | 49503.50 | 0 |

| 2 | 2 | 15694510 | 1217 | 678 | 0 | 1 | 40.0 | 10 | 0.00 | 2 | 1.0 | 0.0 | 184866.69 | 0 |

| 3 | 3 | 15741417 | 1341 | 581 | 0 | 1 | 34.0 | 2 | 148882.54 | 1 | 1.0 | 1.0 | 84560.88 | 0 |

| 4 | 4 | 15766172 | 483 | 716 | 2 | 1 | 33.0 | 5 | 0.00 | 2 | 1.0 | 1.0 | 15068.83 | 0 |

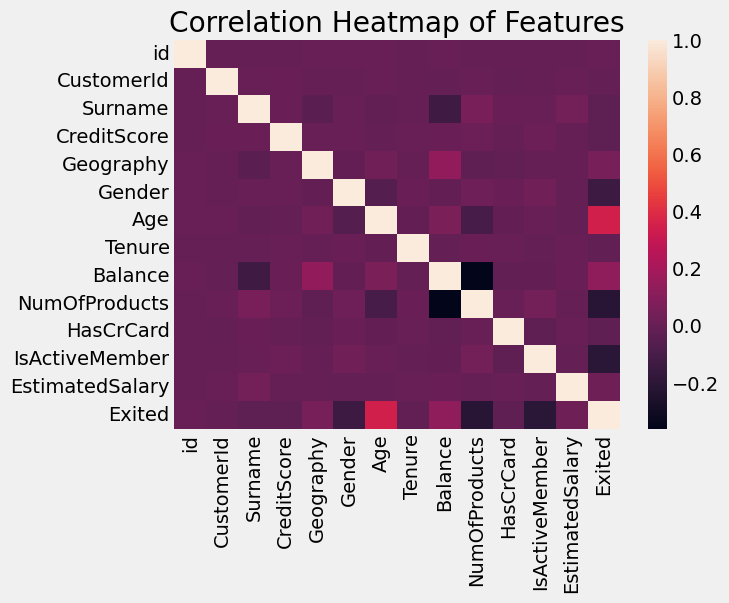

sns.heatmap(df.corr(numeric_only=True))

plt.title('Correlation Heatmap of Features')

plt.show()

Looking at linear correlation coefficients we see that Age and NumOfProducts have the largest effect on churn

4. Feature Engineering

# Feature engineering

df_eng = df.copy()

# Customer above age of retirement of the 3 countries in dataset

df_eng.loc[df_eng['Age']>=60, 'SeniorAge'] = 1

df_eng.loc[df_eng['Age']<60, 'SeniorAge'] = 0

# Customer is still young

df_eng.loc[df_eng['Age']<=35, 'Young'] = 1

df_eng.loc[df_eng['Age']>35, 'Young'] = 0

# Ratio of Balance and Estimated Salary

df_eng['Ratio_Bal_Sal'] = df_eng['Balance']/df_eng['EstimatedSalary']

# Ratio of Balance and Age

df_eng['Ratio_Bal_Age'] = df_eng['Balance']/df_eng['Age']

# Ratio of Estimated Salary and Age

df_eng['Ratio_Sal_Age'] = df_eng['EstimatedSalary']/df_eng['Age']

# Ratio of Tenure and NumOfProducts

df_eng['Ratio_Ten_Num'] = df_eng['Tenure']/df_eng['NumOfProducts']

# CreditScore bin

df_eng['Bin_CreditScore'] = pd.cut(df_eng['CreditScore'], bins=[0, 600, 700, 900], labels=[0,1,2]).astype(int)

# Age bin

df_eng['Bin_Age'] = df_eng['Age']//10

df_eng.head()

| id | CustomerId | Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | ... | EstimatedSalary | Exited | SeniorAge | Young | Ratio_Bal_Sal | Ratio_Bal_Age | Ratio_Sal_Age | Ratio_Ten_Num | Bin_CreditScore | Bin_Age | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 15674932 | 1992 | 668 | 0 | 1 | 33.0 | 3 | 0.00 | 2 | ... | 181449.97 | 0 | 0.0 | 1.0 | 0.000000 | 0.000000 | 5498.483939 | 1.5 | 1 | 3.0 |

| 1 | 1 | 15749177 | 1993 | 627 | 0 | 1 | 33.0 | 1 | 0.00 | 2 | ... | 49503.50 | 0 | 0.0 | 1.0 | 0.000000 | 0.000000 | 1500.106061 | 0.5 | 1 | 3.0 |

| 2 | 2 | 15694510 | 1217 | 678 | 0 | 1 | 40.0 | 10 | 0.00 | 2 | ... | 184866.69 | 0 | 0.0 | 0.0 | 0.000000 | 0.000000 | 4621.667250 | 5.0 | 1 | 4.0 |

| 3 | 3 | 15741417 | 1341 | 581 | 0 | 1 | 34.0 | 2 | 148882.54 | 1 | ... | 84560.88 | 0 | 0.0 | 1.0 | 1.760655 | 4378.898235 | 2487.084706 | 2.0 | 0 | 3.0 |

| 4 | 4 | 15766172 | 483 | 716 | 2 | 1 | 33.0 | 5 | 0.00 | 2 | ... | 15068.83 | 0 | 0.0 | 1.0 | 0.000000 | 0.000000 | 456.631212 | 2.5 | 2 | 3.0 |

5 rows × 22 columns

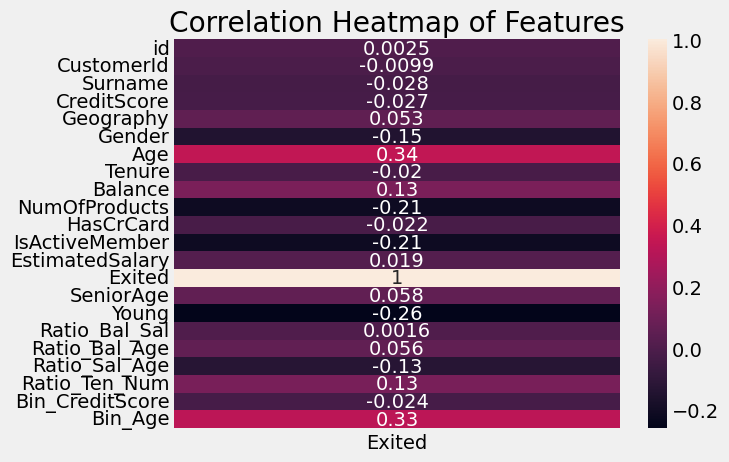

Above are some simple features that were created to transform some of the features to help with our model’s learning. These could be through inspiration and knowledge of the domain or simply random numerical transformations.

df_eng.corr()[['Exited']].index

Index(['id', 'CustomerId', 'Surname', 'CreditScore', 'Geography', 'Gender',

'Age', 'Tenure', 'Balance', 'NumOfProducts', 'HasCrCard',

'IsActiveMember', 'EstimatedSalary', 'Exited', 'SeniorAge', 'Young',

'Ratio_Bal_Sal', 'Ratio_Bal_Age', 'Ratio_Sal_Age', 'Ratio_Ten_Num',

'Bin_CreditScore', 'Bin_Age'],

dtype='object')

sns.heatmap(df_eng.corr()[['Exited']], annot=True, yticklabels=df_eng.corr()[['Exited']].index)

plt.title('Correlation Heatmap of Features')

plt.show()

X_train = df_eng.drop(['id','CustomerId','Exited'], axis=1)

X_train.head()

| Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | SeniorAge | Young | Ratio_Bal_Sal | Ratio_Bal_Age | Ratio_Sal_Age | Ratio_Ten_Num | Bin_CreditScore | Bin_Age | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1992 | 668 | 0 | 1 | 33.0 | 3 | 0.00 | 2 | 1.0 | 0.0 | 181449.97 | 0.0 | 1.0 | 0.000000 | 0.000000 | 5498.483939 | 1.5 | 1 | 3.0 |

| 1 | 1993 | 627 | 0 | 1 | 33.0 | 1 | 0.00 | 2 | 1.0 | 1.0 | 49503.50 | 0.0 | 1.0 | 0.000000 | 0.000000 | 1500.106061 | 0.5 | 1 | 3.0 |

| 2 | 1217 | 678 | 0 | 1 | 40.0 | 10 | 0.00 | 2 | 1.0 | 0.0 | 184866.69 | 0.0 | 0.0 | 0.000000 | 0.000000 | 4621.667250 | 5.0 | 1 | 4.0 |

| 3 | 1341 | 581 | 0 | 1 | 34.0 | 2 | 148882.54 | 1 | 1.0 | 1.0 | 84560.88 | 0.0 | 1.0 | 1.760655 | 4378.898235 | 2487.084706 | 2.0 | 0 | 3.0 |

| 4 | 483 | 716 | 2 | 1 | 33.0 | 5 | 0.00 | 2 | 1.0 | 1.0 | 15068.83 | 0.0 | 1.0 | 0.000000 | 0.000000 | 456.631212 | 2.5 | 2 | 3.0 |

y_train = df_eng['Exited']

y_train.head()

0 0

1 0

2 0

3 0

4 0

Name: Exited, dtype: int64

class AddClustersFeature(BaseEstimator, TransformerMixin):

def __init__(self, clusters = 8):

self.clusters = clusters

def fit(self, X, y=None):

self.X=X

self.model = KMeans(n_clusters = self.clusters)

self.model.fit (self.X)

return self

def transform(self, X):

self.X=X

X_=X.copy() # avoiding modification of the original df

X_ = pd.DataFrame(X_)

X_['Clusters'] = self.model.predict(X_)

X_.columns = X_.columns.astype(str)

#print(X_.info())

return X_

# Sanity check that function to add cluster as a feature works

cluster_sanity = X_train.copy()

m = AddClustersFeature()

m.fit(cluster_sanity)

cluster_sanity = m.transform(cluster_sanity)

cluster_sanity.head()

| Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | SeniorAge | Young | Ratio_Bal_Sal | Ratio_Bal_Age | Ratio_Sal_Age | Ratio_Ten_Num | Bin_CreditScore | Bin_Age | Clusters | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1992 | 668 | 0 | 1 | 33.0 | 3 | 0.00 | 2 | 1.0 | 0.0 | 181449.97 | 0.0 | 1.0 | 0.000000 | 0.000000 | 5498.483939 | 1.5 | 1 | 3.0 | 3 |

| 1 | 1993 | 627 | 0 | 1 | 33.0 | 1 | 0.00 | 2 | 1.0 | 1.0 | 49503.50 | 0.0 | 1.0 | 0.000000 | 0.000000 | 1500.106061 | 0.5 | 1 | 3.0 | 4 |

| 2 | 1217 | 678 | 0 | 1 | 40.0 | 10 | 0.00 | 2 | 1.0 | 0.0 | 184866.69 | 0.0 | 0.0 | 0.000000 | 0.000000 | 4621.667250 | 5.0 | 1 | 4.0 | 3 |

| 3 | 1341 | 581 | 0 | 1 | 34.0 | 2 | 148882.54 | 1 | 1.0 | 1.0 | 84560.88 | 0.0 | 1.0 | 1.760655 | 4378.898235 | 2487.084706 | 2.0 | 0 | 3.0 | 7 |

| 4 | 483 | 716 | 2 | 1 | 33.0 | 5 | 0.00 | 2 | 1.0 | 1.0 | 15068.83 | 0.0 | 1.0 | 0.000000 | 0.000000 | 456.631212 | 2.5 | 2 | 3.0 | 4 |

Through clustering of our data points, another engineered feature can be added to our dataset. Depending on the clustering algorithm it can provide different additional information about our data points. In this case we are using KMeans which attempts to group similar datapoints based on their Euclidean distances.

5. Modelling

#################################################################

# Instantiate models and params

logreg = LogisticRegression(random_state = 47)

logreg_params = {'C': np.logspace(-4, 4, 6),

'solver': ['lbfgs','newton-cg','sag','saga']

}

rfc = RandomForestClassifier(random_state = 47)

rfc_params = {'n_estimators': [10,50,100],

'min_samples_split': [2, 5, 10, 20]

}

xgb = XGBClassifier(random_state = 47,

objective='binary:logistic',

metric='auc',

device = 'cuda', error_score='raise')

xgb_params = {'eta': [0.01,0.1,0.3],

'max_depth': [3,6,9],

'lambda': [0.3,0.6,1],

'alpha': [0,0.1],

'min_child_weight': [1,10,20],

'colsample_bytree': [0.25,0.5,1]

}

lgb = LGBMClassifier(random_state = 47,

objective='binary',

metric='auc',

verbosity=-1)

lgb_params = {'max_bin': [10,69,150,255,400],

'max_depth': [3,6,9],

'learning_rate': [ 0.01, 0.1],

'lambda_l1': [0,0.1],

'lambda_l2': [0,0.3,0.6],

'num_leaves': [10,31,50]

}

clfs = [

('Logistic Regression', logreg, logreg_params),

('Random Forest Classifier', rfc, rfc_params),

('XGBoost Classifier', xgb, xgb_params),

('LGBM Classifier', lgb, lgb_params)

]

scorers = {

'accuracy_score': make_scorer(accuracy_score),

'f1_score': make_scorer(f1_score),

'roc_auc_score': make_scorer(roc_auc_score)

}

# Compare model performance of (all features) vs (all w/o cluster features) vs (all w/o cluster+surname features) vs (w/o scaling) using xgb

X_train_nosurname = X_train.drop('Surname',axis=1)

pipeline = Pipeline(steps = [

('scaler', MinMaxScaler()),

('cluster', AddClustersFeature()),

('xgb', xgb)

])

pipeline_noclust = Pipeline(steps=[

('scaler', MinMaxScaler()),

('xgb', xgb)

])

pipeline_noscale = Pipeline(steps=[

('cluster', AddClustersFeature()),

('xgb', xgb)

])

pipelines = [('Pipeline', pipeline), ('Pipeline_No_Cluster', pipeline_noclust), ('Pipeline_No_Scale', pipeline_noscale)]

results = []

cv = KFold(n_splits=5)

for pipe_name, pipe in pipelines:

scores = cross_val_score(estimator=pipe, X=X_train, y=y_train, cv=cv, scoring='roc_auc')

results.append(scores)

scores = cross_val_score(estimator=pipe, X=X_train_nosurname, y=y_train, cv=cv, scoring='roc_auc')

results.append(scores)

Here we are fitting an XGBoost model in several different scenarios to find our best performing scenario. Below are the scenarios:

- Dataset is scaled and cluster feature added

- Dataset is scaled

- Dataset has cluster feature added This is repeated for training data with and without Surname feature for a total of 6 different scenarios.

best_result = [-1, 0]

for idx, result in enumerate(results):

mean_result = np.mean(result)

print(f'Pipeline: {idx}, Mean ROC AUC: {mean_result}')

if mean_result > best_result[1]:

best_result = [idx, mean_result]

print(f' Best pipeline is {best_result[0]} with a mean score of {best_result[1]}')

# Best performer is dataset including Surname, with feature scaling and additional cluster feature included

Pipeline: 0, Mean ROC AUC: 0.8888409253562118

Pipeline: 1, Mean ROC AUC: 0.8859394416907461

Pipeline: 2, Mean ROC AUC: 0.8886329403159834

Pipeline: 3, Mean ROC AUC: 0.8858966559943475

Pipeline: 4, Mean ROC AUC: 0.8887585013508655

Pipeline: 5, Mean ROC AUC: 0.8862002696202766

Best pipeline is 0 with a mean score of 0.8888409253562118

Best performer after 5 fold cross validation is Dataset+Surname feature with feature scaling and cluster feature included. This is the scenario that we will be tuning our final models on.

# Pipeline

results = []

for clf_name, clf, clf_params in clfs:

gs = GridSearchCV(estimator=clf,

param_grid=clf_params,

scoring=scorers,

refit='roc_auc_score',

verbose=2,

error_score='raise'

)

pipeline = Pipeline(steps=[

('scaler', MinMaxScaler()),

('cluster', AddClustersFeature()),

('classifier', gs),

])

pipeline.fit(X_train, y_train)

result = [clf_name, gs.best_params_, gs.best_score_, gs.cv_results_['mean_test_f1_score'][gs.best_index_], gs.cv_results_['mean_test_accuracy_score'][gs.best_index_]]

results.append(result)

result_df = pd.DataFrame(results, columns=['Name','Parameters','ROCAUC','F1','Accuracy'])

result_df.head()

Fitting 5 folds for each of 24 candidates, totalling 120 fits

Fitting 5 folds for each of 12 candidates, totalling 60 fits

Fitting 5 folds for each of 486 candidates, totalling 2430 fits

Fitting 5 folds for each of 540 candidates, totalling 2700 fits

| Name | Parameters | ROCAUC | F1 | Accuracy | |

|---|---|---|---|---|---|

| 0 | Logistic Regression | {'C': 6.309573444801943, 'solver': 'lbfgs'} | 0.671971 | 0.498950 | 0.833295 |

| 1 | Random Forest Classifier | {'min_samples_split': 20, 'n_estimators': 100} | 0.742522 | 0.622877 | 0.863489 |

| 2 | XGBoost Classifier | {'alpha': 0, 'colsample_bytree': 1, 'eta': 0.3... | 0.755960 | 0.641102 | 0.866179 |

| 3 | LGBM Classifier | {'lambda_l1': 0, 'lambda_l2': 0.6, 'learning_r... | 0.755667 | 0.641445 | 0.866840 |

Out of the 4 models tuned, XGB and LGBM classifiers have the best performance. As their performance are similar, we shall go one step further and create a final voting classifier to make use of both best performers.

result_df[result_df['Name'].isin(['XGBoost Classifier','LGBM Classifier'])]['Parameters'].tolist()

[{'alpha': 0,

'colsample_bytree': 1,

'eta': 0.3,

'lambda': 0.6,

'max_depth': 6,

'min_child_weight': 1},

{'lambda_l1': 0,

'lambda_l2': 0.6,

'learning_rate': 0.1,

'max_bin': 400,

'max_depth': 6,

'num_leaves': 31}]

########################################################################################

xgb = XGBClassifier(random_state = 47,

objective='binary:logistic',

metric='auc',

device = 'cuda',

alpha= 0,

colsample_bytree= 1,

eta= 0.3,

reg_lambda= 0.6,

max_depth= 6,

min_child_weight= 1,

error_score='raise')

lgb = LGBMClassifier(random_state = 47,

objective='binary',

metric='auc',

verbosity=-1,

lambda_l1= 0,

lambda_l2= 0.6,

learning_rate= 0.1,

max_bin= 400,

max_depth= 6,

num_leaves= 31)

vc = VotingClassifier(estimators=[('xgb',xgb),('lgb',lgb)], voting='soft')

X_train.head()

| Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | SeniorAge | Young | Ratio_Bal_Sal | Ratio_Bal_Age | Ratio_Sal_Age | Ratio_Ten_Num | Bin_CreditScore | Bin_Age | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1992 | 668 | 0 | 1 | 33.0 | 3 | 0.00 | 2 | 1.0 | 0.0 | 181449.97 | 0.0 | 1.0 | 0.000000 | 0.000000 | 5498.483939 | 1.5 | 1 | 3.0 |

| 1 | 1993 | 627 | 0 | 1 | 33.0 | 1 | 0.00 | 2 | 1.0 | 1.0 | 49503.50 | 0.0 | 1.0 | 0.000000 | 0.000000 | 1500.106061 | 0.5 | 1 | 3.0 |

| 2 | 1217 | 678 | 0 | 1 | 40.0 | 10 | 0.00 | 2 | 1.0 | 0.0 | 184866.69 | 0.0 | 0.0 | 0.000000 | 0.000000 | 4621.667250 | 5.0 | 1 | 4.0 |

| 3 | 1341 | 581 | 0 | 1 | 34.0 | 2 | 148882.54 | 1 | 1.0 | 1.0 | 84560.88 | 0.0 | 1.0 | 1.760655 | 4378.898235 | 2487.084706 | 2.0 | 0 | 3.0 |

| 4 | 483 | 716 | 2 | 1 | 33.0 | 5 | 0.00 | 2 | 1.0 | 1.0 | 15068.83 | 0.0 | 1.0 | 0.000000 | 0.000000 | 456.631212 | 2.5 | 2 | 3.0 |

# Scaling and adding cluster on full training data

scaler = MinMaxScaler()

X_train_final = X_train.copy()

X_train_final = scaler.fit_transform(X_train_final)

X_train_final = AddClustersFeature().fit_transform(X_train_final)

X_train_final

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | Clusters | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.689751 | 0.636 | 0.0 | 1.0 | 0.202703 | 0.3 | 0.000000 | 0.333333 | 1.0 | 0.0 | 0.907279 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.496366 | 0.15 | 0.5 | 0.250 | 6 |

| 1 | 0.690097 | 0.554 | 0.0 | 1.0 | 0.202703 | 0.1 | 0.000000 | 0.333333 | 1.0 | 1.0 | 0.247483 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.135405 | 0.05 | 0.5 | 0.250 | 3 |

| 2 | 0.421399 | 0.656 | 0.0 | 1.0 | 0.297297 | 1.0 | 0.000000 | 0.333333 | 1.0 | 0.0 | 0.924364 | 0.0 | 0.0 | 0.000000 | 0.000000 | 0.417210 | 0.50 | 0.5 | 0.375 | 0 |

| 3 | 0.464335 | 0.462 | 0.0 | 1.0 | 0.216216 | 0.2 | 0.593398 | 0.000000 | 1.0 | 1.0 | 0.422787 | 0.0 | 1.0 | 0.000137 | 0.424012 | 0.224506 | 0.20 | 0.0 | 0.250 | 3 |

| 4 | 0.167244 | 0.732 | 1.0 | 1.0 | 0.202703 | 0.5 | 0.000000 | 0.333333 | 1.0 | 1.0 | 0.075293 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.041203 | 0.25 | 1.0 | 0.250 | 3 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 165029 | 0.608726 | 0.634 | 1.0 | 0.0 | 0.202703 | 0.2 | 0.000000 | 0.000000 | 1.0 | 1.0 | 0.659179 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.360636 | 0.20 | 0.5 | 0.250 | 1 |

| 165030 | 0.687673 | 0.884 | 0.0 | 1.0 | 0.229730 | 0.3 | 0.000000 | 0.000000 | 0.0 | 0.0 | 0.659177 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.340026 | 0.30 | 1.0 | 0.250 | 6 |

| 165031 | 0.419321 | 0.430 | 0.0 | 1.0 | 0.175676 | 0.5 | 0.000000 | 0.000000 | 1.0 | 1.0 | 0.637151 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.371075 | 0.50 | 0.0 | 0.250 | 3 |

| 165032 | 0.420706 | 0.408 | 1.0 | 0.0 | 0.162162 | 0.7 | 0.643819 | 0.000000 | 0.0 | 1.0 | 0.355841 | 0.0 | 1.0 | 0.000176 | 0.521378 | 0.214156 | 0.70 | 0.0 | 0.250 | 1 |

| 165033 | 0.916898 | 1.000 | 0.0 | 1.0 | 0.175676 | 0.1 | 0.000000 | 0.000000 | 1.0 | 0.0 | 0.307880 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.179316 | 0.10 | 1.0 | 0.250 | 6 |

165034 rows × 20 columns

cross_val_score(vc, X_train_final, y_train, scoring='roc_auc')

array([0.8940815 , 0.88922709, 0.89204022, 0.89081926, 0.8903584 ])

Above shows our expected model performance if our model did not overfit and trainin/test data share similar distributions

vc.fit(X_train_final, y_train)

VotingClassifier(estimators=[('xgb',

XGBClassifier(alpha=0, base_score=None,

booster=None, callbacks=None,

colsample_bylevel=None,

colsample_bynode=None,

colsample_bytree=1, device='cuda',

early_stopping_rounds=None,

enable_categorical=False,

error_score='raise', eta=0.3,

eval_metric=None,

feature_types=None, gamma=None,

grow_policy=None,

importance_type=None,

inter...

learning_rate=None, max_bin=None,

max_cat_threshold=None,

max_cat_to_onehot=None,

max_delta_step=None, max_depth=6,

max_leaves=None, metric='auc',

min_child_weight=1, missing=nan,

monotone_constraints=None,

multi_strategy=None, ...)),

('lgb',

LGBMClassifier(lambda_l1=0, lambda_l2=0.6,

max_bin=400, max_depth=6,

metric='auc', objective='binary',

random_state=47, verbosity=-1))],

voting='soft')In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

VotingClassifier(estimators=[('xgb',

XGBClassifier(alpha=0, base_score=None,

booster=None, callbacks=None,

colsample_bylevel=None,

colsample_bynode=None,

colsample_bytree=1, device='cuda',

early_stopping_rounds=None,

enable_categorical=False,

error_score='raise', eta=0.3,

eval_metric=None,

feature_types=None, gamma=None,

grow_policy=None,

importance_type=None,

inter...

learning_rate=None, max_bin=None,

max_cat_threshold=None,

max_cat_to_onehot=None,

max_delta_step=None, max_depth=6,

max_leaves=None, metric='auc',

min_child_weight=1, missing=nan,

monotone_constraints=None,

multi_strategy=None, ...)),

('lgb',

LGBMClassifier(lambda_l1=0, lambda_l2=0.6,

max_bin=400, max_depth=6,

metric='auc', objective='binary',

random_state=47, verbosity=-1))],

voting='soft')XGBClassifier(alpha=0, base_score=None, booster=None, callbacks=None,

colsample_bylevel=None, colsample_bynode=None, colsample_bytree=1,

device='cuda', early_stopping_rounds=None,

enable_categorical=False, error_score='raise', eta=0.3,

eval_metric=None, feature_types=None, gamma=None,

grow_policy=None, importance_type=None,

interaction_constraints=None, learning_rate=None, max_bin=None,

max_cat_threshold=None, max_cat_to_onehot=None,

max_delta_step=None, max_depth=6, max_leaves=None, metric='auc',

min_child_weight=1, missing=nan, monotone_constraints=None,

multi_strategy=None, ...)LGBMClassifier(lambda_l1=0, lambda_l2=0.6, max_bin=400, max_depth=6,

metric='auc', objective='binary', random_state=47, verbosity=-1)# Preparing test data for prediction

test_df = pd.read_csv('test.csv')

test_df.head()

| id | CustomerId | Surname | CreditScore | Geography | Gender | Age | Tenure | Balance | NumOfProducts | HasCrCard | IsActiveMember | EstimatedSalary | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 165034 | 15773898 | Lucchese | 586 | France | Female | 23.0 | 2 | 0.00 | 2 | 0.0 | 1.0 | 160976.75 |

| 1 | 165035 | 15782418 | Nott | 683 | France | Female | 46.0 | 2 | 0.00 | 1 | 1.0 | 0.0 | 72549.27 |

| 2 | 165036 | 15807120 | K? | 656 | France | Female | 34.0 | 7 | 0.00 | 2 | 1.0 | 0.0 | 138882.09 |

| 3 | 165037 | 15808905 | O'Donnell | 681 | France | Male | 36.0 | 8 | 0.00 | 1 | 1.0 | 0.0 | 113931.57 |

| 4 | 165038 | 15607314 | Higgins | 752 | Germany | Male | 38.0 | 10 | 121263.62 | 1 | 1.0 | 0.0 | 139431.00 |

test_df.shape

(110023, 13)

test_df['Geography'].unique()

array(['France', 'Germany', 'Spain'], dtype=object)

X_train_final.shape

(165034, 20)

# Encoding categorical features

test_df['Geography'] = le_geo.transform(test_df['Geography'])

test_df['Gender'] = le_gender.transform(test_df['Gender'])

test_df['Surname'] = le_surname.transform(test_df['Surname'])

test_df.head()

# Customer above age of retirement of the 3 countries in dataset

test_df.loc[test_df['Age']>=60, 'SeniorAge'] = 1

test_df.loc[test_df['Age']<60, 'SeniorAge'] = 0

# Customer is still young

test_df.loc[test_df['Age']<=35, 'Young'] = 1

test_df.loc[test_df['Age']>35, 'Young'] = 0

# Ratio of Balance and Estimated Salary

test_df['Ratio_Bal_Sal'] = test_df['Balance']/test_df['EstimatedSalary']

# Ratio of Balance and Age

test_df['Ratio_Bal_Age'] = test_df['Balance']/test_df['Age']

# Ratio of Estimated Salary and Age

test_df['Ratio_Sal_Age'] = test_df['EstimatedSalary']/test_df['Age']

# Ratio of Tenure and NumOfProducts

test_df['Ratio_Ten_Num'] = test_df['Tenure']/test_df['NumOfProducts']

# CreditScore bin

test_df['Bin_CreditScore'] = pd.cut(test_df['CreditScore'], bins=[0, 600, 700, 900], labels=[0,1,2]).astype(int)

# Age bin

test_df['Bin_Age'] = test_df['Age']//10

# Save id to join with final predictions

idx = test_df['id']

X_test = test_df.drop(['id','CustomerId'], axis=1)

# Scale features and add clusters

X_test = scaler.transform(X_test)

X_test = m.transform(X_test)

X_test.head()

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | Clusters | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.547438 | 0.472 | 0.0 | 0.0 | 0.067568 | 0.2 | 0.000000 | 0.333333 | 0.0 | 1.0 | 0.804903 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.631827 | 0.10 | 0.0 | 0.125 | 4 |

| 1 | 0.670014 | 0.666 | 0.0 | 0.0 | 0.378378 | 0.2 | 0.000000 | 0.000000 | 1.0 | 0.0 | 0.362723 | 0.0 | 0.0 | 0.000000 | 0.000000 | 0.142361 | 0.20 | 0.5 | 0.375 | 4 |

| 2 | 0.460873 | 0.612 | 0.0 | 0.0 | 0.216216 | 0.7 | 0.000000 | 0.333333 | 1.0 | 0.0 | 0.694419 | 0.0 | 1.0 | 0.000000 | 0.000000 | 0.368740 | 0.35 | 0.5 | 0.250 | 4 |

| 3 | 0.676939 | 0.662 | 0.0 | 1.0 | 0.243243 | 0.8 | 0.000000 | 0.000000 | 1.0 | 0.0 | 0.569654 | 0.0 | 0.0 | 0.000000 | 0.000000 | 0.285685 | 0.80 | 0.5 | 0.250 | 4 |

| 4 | 0.399238 | 0.804 | 0.5 | 1.0 | 0.270270 | 1.0 | 0.483318 | 0.000000 | 1.0 | 0.0 | 0.697164 | 0.0 | 0.0 | 0.000068 | 0.309001 | 0.331227 | 1.00 | 1.0 | 0.250 | 4 |

# Make and export predictions in format for submission

y_pred = vc.predict_proba(X_test)[:, 1]

predictions = pd.concat([idx, pd.Series(y_pred)], axis=1)

predictions.columns = 'id','Exited'

predictions.to_csv('predictions_.csv', index=False)

predictions

| id | Exited | |

|---|---|---|

| 0 | 165034 | 0.043242 |

| 1 | 165035 | 0.856776 |

| 2 | 165036 | 0.027904 |

| 3 | 165037 | 0.242382 |

| 4 | 165038 | 0.358144 |

| ... | ... | ... |

| 110018 | 275052 | 0.030970 |

| 110019 | 275053 | 0.154990 |

| 110020 | 275054 | 0.023756 |

| 110021 | 275055 | 0.160589 |

| 110022 | 275056 | 0.196556 |

110023 rows × 2 columns

Our predictions currently has a public score of 0.88895 after submission, which is close to what we have expected.

6. Conclusion

In this notebook we have explored a synthetic bank churn dataset and briefly discussed what could be done differently in a real world scenario. With a churn rate of ~21% our model has an ROCAUC of 0.88895 which appears to be a relatively good performance that beats out a random guess strategy. With some domain knowledge or time investment, one can create certain conditional strategies that predicts customer churn. Further analysis between the predictive model and those conditional strategies will then tell us if the model performance is indeed worthwhile.